Fitch: Egypt’s FY2022 budgetary targets as ‘broadly credible’

Fitch Ratings describe Egypt’s budgetary targets for the the financial year ending June 2022 (FY22) as “broadly credible.”

The rating agency said in a recent report that Egypt’s new draft budget continues the government’s fiscal and economic reform agenda, which is critical to reducing its high debt burden over the medium term.

The budget envisages the central government overall deficit falling to 6.7 percent of GDP in FY22, from an estimated 7.9 percent in FY21. The deficit of the broader general government (GG), which tends to be narrower, is likely to end up below our previous projections of 8.5 percent of GDP in FY22 and 6.9 percent of GDP in FY21.

The estimated FY21 deficit already represents significant overperformance against projections in Egypt’s IMF programme, Fitch added.

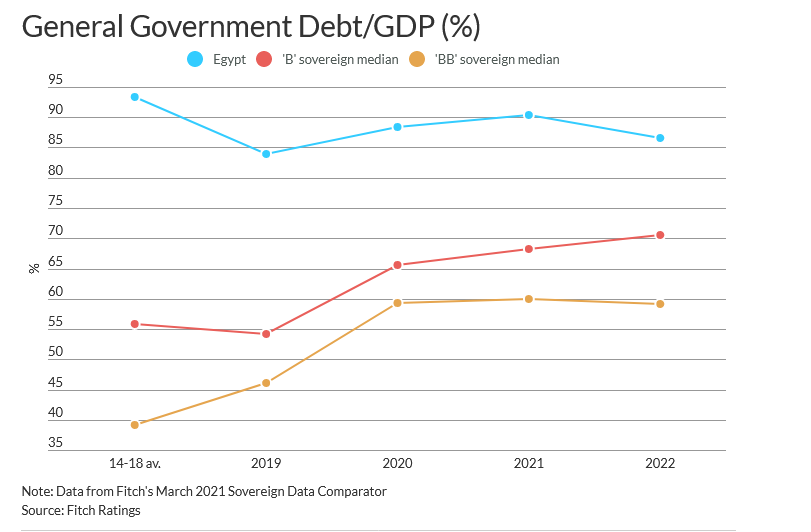

“We believe Egypt’s budgetary targets are broadly credible. The budget outperformed government projections in FY19, and underperformance in FY20-FY21 has been modest – given the scale of the COVID-19 shock. The pandemic interrupted progress on debt reduction, and public finances remain a core weakness of the rating. However, we expect that GG debt will resume a downward path in FY22 after rising from 84 percent of GDP in FY19 to 90 percent in FY21.”

According to Fitch, more than half of GG external debt is owed to multilateral institutions, with which Egypt has good relations, and the domestic banking sector provides a captive investor base for local-currency debt. “This, and Egypt’s broad financing options, mitigate the associated credit risks.”

“When we affirmed Egypt’s B+/Stable rating in March, we said that positive rating action could result from sustained progress on fiscal consolidation, leading to a further substantial reduction over the medium term in debt/GDP and bringing it closer to the ‘B’ median.”

The budget shifts the focus of spending towards capital projects, which may support long-term growth potential, Fitch noted.

The Egyptian government plans to increase capital spending to 5 percent of GDP in FY22, from 3.6 percent in FY21 and 3.3 percent in FY20. This is funded partly by an increase in other non-tax revenues, which includes revenue raised by self-funding entities.

Elsewhere, Fitch said the budget projects that wage and salary expenditure will stay flat as a share of GDP (as it has since FY19), reflecting restraint in hiring and modest increases in real pay.

“Most other spending declines, helped by the roll-off of coronavirus-related spending, which amounted to nearly 1 percent of GDP in FY21. Interest costs are also set to fall, mainly as a result of lower policy interest rates.”

Th rating agency further said the tax revenue is to rise to 13.9 percent of GDP in FY22, from 13 percent in FY21 and 12.7 percent in FY20.

“This is in line with the government’s intention to raise tax revenue/GDP by 2pp between FY21 and FY24 through reforms to the tax structure and improved administration, outlined in its Medium-Term Revenue Strategy. The government has struggled to raise revenue/GDP in recent years, but the FY21 revenue estimates point to progress. “

The budget projects a 7.1 percent increase in the government’s funding requirement, to $68 billion, most of which would be covered by domestic funding (the equivalent of $63 billion). This could be hard to absorb without further increases in non-resident participation in Egypt’s local-currency bond market, the report added.

“Foreign investor participation in Egypt’s bond market is a growing point of potential external vulnerability, even as it supports fiscal and current-account funding. Foreign holdings of government T-bills and T-bonds had recovered to $28 billion by February 2021, accounting for over 10 percent of government domestic debt, from less than $10 billion in June 2020.”

“Egypt’s attractive real interest rates, relatively strong economic performance, expected JP Morgan index inclusion and Euroclearability could attract further inflows. However, these flows could quickly reverse in response to shocks affecting investor confidence, putting pressure on Egypt’s foreign-exchange liquidity, interest rates and the exchange rate.”