Egypt’s non-oil private sector expands in Jan

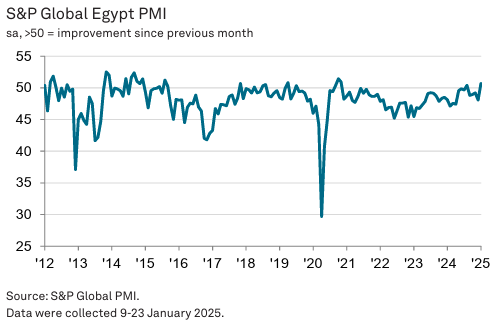

Egypt’s non-oil private sector returned to growth in January, with the Purchasing Managers’ Index (PMI) jumping to 50.7, up from 48.1 in December, marking its highest level since November 2020, according to S&P Global.

The expansion, following a prolonged downturn, was driven by a rise in output and new orders, supported by improving domestic demand and easing cost pressures.

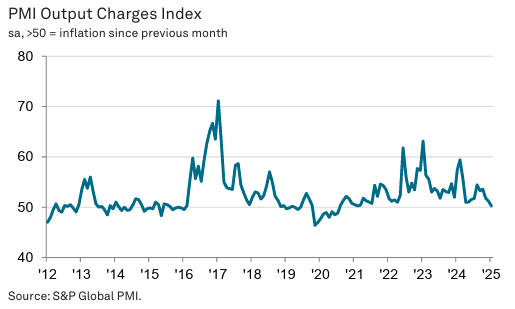

The data signalled a shift in market conditions, with firms reporting increased sales, particularly in manufacturing, construction, and retail, while the services sector saw a decline. Businesses attributed the rebound to softening input cost inflation, as some material prices fell, contributing to a slowdown in output price inflation to its lowest in four-and-a-half years.

Employment

Employment levels stabilised in January, following two months of job cuts. While some firms hired additional workers to meet rising sales demand, reductions in staffing elsewhere kept overall employment unchanged. Despite the increased activity, firms were cautious about expanding their workforce due to uncertainty about the longevity of the recovery.

A more stable supply chain also supported business activity, with delivery times remaining steady. Although overall input prices continued to rise, inflationary pressures eased to an eight-month low. Some firms faced higher costs due to a stronger US dollar, while others benefited from declining material prices, particularly in construction, which recorded a drop in purchase costs.

Outlook

Despite signs of recovery, firms remained cautious about the outlook, with business expectations slipping to a historically low level. Concerns over economic stability, currency fluctuations, and geopolitical uncertainty tempered optimism, leading many firms to take a wait-and-see approach. While easing inflation and improved demand offer positive momentum, businesses remain hesitant about expanding operations or increasing hiring until a more sustained recovery is evident.

Attribution: Amwal Al Ghad English

Subediting: M. S. Salama